We’re two months into 2021 and have officially closed the door on an unforgettable 2020. So, how did retailers and brands do? Let’s take a closer look.

Going into peak season, we knew that ecommerce was going to play a much larger role than in years past. We saw the signs early: According to a Rithum holiday survey, 83% of shoppers planned to do most or all their shopping online. This is a big shift when you consider that it’s a 40% increase compared to last year when 59% of consumers said that they would be doing more than half of their holiday shopping online. But were brands and retailers ready?

The big theme for this past peak was “pulling demand earlier.” In other words, enticing shoppers to start shopping sooner and offering deals over a longer stretch of the peak season. Most major retailers, carriers, and marketplaces all stressed this as a strategy to maximize sales while minimizing the strain on fulfillment and logistics. As a result, peak season started earlier than in prior years. While good in theory, it ushered in some major changes with regards to logistics and parcel volume restrictions that could have an impact for some time to come. What do we mean by that?

Logistics Gets a Price Increase

Retailers and online marketplaces were not the only players in the space that were going to be impacted. Carriers were going to need to manage a significantly larger volume of packages throughout that time period. As a result, carriers took steps to mitigate those impacts and protect their ability to perform at their historical service levels. Increased parcel volume was not a surprise at all. Throughout the last half of the year, we were vocal about what we saw coming in peak (read our blog: What Retailers and Brands Need to Know to Prepare for the Second Half of 2020.)

As volumes continued to grow, additional resources were necessary to increase carrier capacity. The associated costs of this increase could not be covered only by the carriers, so they implemented additional fees to help offset those costs. Here’s a summary of some of those changes:

- UPS. Took several steps to implement fees, whether it was modifications to the dim/weight calculation, reducing the weight for oversized packages, or simply adding additional surcharges for volume throughout peak season.

- FedEx Ground. Beginning on October 5, which made the additional cost applicable over Prime Day, FedEx added a Peak – Additional Handling Surcharge of $4.90 per package that remained in place until January 17 of this year. Regardless of your negotiated rates with FedEx, this is a significant increase to the cost of shipping. Their other discount ship method, FedEx SmartPost, also saw additional surcharges representing large per order increases as well.

- USPS. Temporarily increased their commercial pricing from October 18 until December 27. USPS Priority Mail, which is popular among Seller Fulfilled Prime shippers when it is available, experienced an almost 6% increase. This ship method is favored for those brands with limited margins, so even increases of this size can make commoditized items less competitive if the item price is increased to compensate.

And, this approach to deal with increased parcel volume doesn’t seem to be ending any time soon as carriers have continued to modify their fee schedule to account for the increased parcel volume. Brands will be forced to choose to slower ship methods or increase prices. In both cases, it’s the consumer that bears the brunt of the impact.

Volume Capacity Limits Held Brands Back

In addition to the surcharges, carriers also put volume limits on shippers. These limitations impacted all level of brands and sellers. As a result of these caps, brands and sellers were forced to make tough decisions with regard to their ecommerce businesses.

With margins already under pressure from the increased shipping costs, shippers sought to maximize the per order margin. Marketplace referral fees are a cost that is not present on a brand’s website so the ability to accommodate that volume while continuing to acquire new customers and engage with repeat customers shifted the availability on marketplaces. The ability to make the shift to .com site is not always available to brands and sellers, nor may it be the best tactical decision. If the .com site does not have the same level of traffic, then this shift is counterproductive.

The ability to be flexible around which channels you enable, with whom you are fulfilling orders, and how you compensate for unexpected costs are all conversations that require insight and planning. Your strategy is not going to be implemented in the weeks leading up to peak season, so having a partner with the foresight and data to anticipate these challenges coupled with the technical capabilities to execute are critical to navigating these impactful changes that occur during critical times of the year. For example, with our expert support we would have advised that brands run digital advertising campaigns to generate demand well in advance of peak.

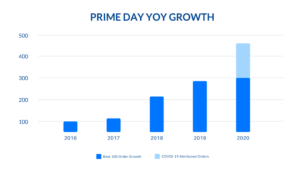

Did Prime Day 2020 Deliver?

We expected that Amazon Prime Day was going to see year-over-year (YoY) growth as social distancing and physical retail disruption generally increased the reliance on ecommerce. Our internal data showed just that with about a third of the order volume on Prime Day being attributed to the COVID-19 impact. Taking it a step further, when adjusting for growth attributable to COVID-19, the 2020 YoY Prime Day growth was only 6%, compared to almost 34% YoY growth from 2018 to 2019. Despite the difference, this was anything but a typical sales period, and sellers and brands benefited from the boost, even if was less than the previous year and much later into the year (Prime Day has traditionally been held in mid-July). In categories where inventory was generally slow to move, any spike in demand as welcome.

Source: Rithum

Prime Day (October 13-14) was Amazon’s official kickoff to the 2020 peak season. Other retailers followed their lead in hopes that they could reduce the stress on the logistics’ networks. The results of those efforts were mixed by category, but ultimately, it appears as though they were generally successful. Consumer electronics, which is a popular category for holiday shoppers saw a significant decrease in YoY sales growth following Thanksgiving. The growth in consumer electronics was deal/promotion driven as retailers continue to ride the Prime Day wave of deal shoppers. Growth post-Thanksgiving was muted, but that was planned, and savvy brands leveraged the early marketing efforts of retailers to ensure they grabbed a share of the early peak buying.

Source: Rithum

After a year like 2020, it is important to take the time to understand what the acceleration of ecommerce means for brands. There’s still a lot of uncertainty as we begin 2021 and the ecommerce supply chain is going to continue to feel the strain. A key area to focus on is distributing inventory across multiple channels as well as shoring up your logistics/carrier partnerships and maximizing your channel strategy to increase sales and offset some of these new limitations.

Check back soon for James’ 2021 outlook with more insight into what lies ahead for brands! And, if you’d like help making your digital supply chain more agile and resilient or strengthening your marketplace strategy, please contact us.